This study material is compiled from a lecture audio transcript and supplementary copy-pasted text.

📚 Accounting and the Business Cycle: A Comprehensive Study Guide

Introduction to Accounting: The Language of Business

Accounting is universally recognized as the "language of business." More precisely, it is a systematic process designed for maintaining detailed reports of a company's operations and effectively communicating that vital information to various decision-makers. The core functions of financial accounting involve two primary aspects:

- ✅ Measuring Business Activities: Meticulously tracking and recording all financial transactions and events.

- ✅ Communicating Information: Presenting the derived information from these activities to facilitate informed decision-making.

Users of Accounting Information

Accounting information serves a diverse group of users, both internal and external, who rely on it for different purposes:

- Internal Users: These are individuals within the organization who use accounting data for strategic planning, operational control, and performance evaluation.

- Directors

- Management

- External Users: These are individuals or entities outside the organization with a vested interest in its financial health and performance.

- Shareholders

- Banks

- Investors

- Clients/Suppliers

- Other stakeholders (e.g., government agencies, employees)

Objective of Financial Statements

The primary objective of financial statements is to circulate transparent and truthful information regarding a company's activities. This includes highlighting both economic and financial aspects, providing a clear and comprehensive picture to all parties interested in the current and prospective management of the company.

📊 The Business Cycle: An Overview

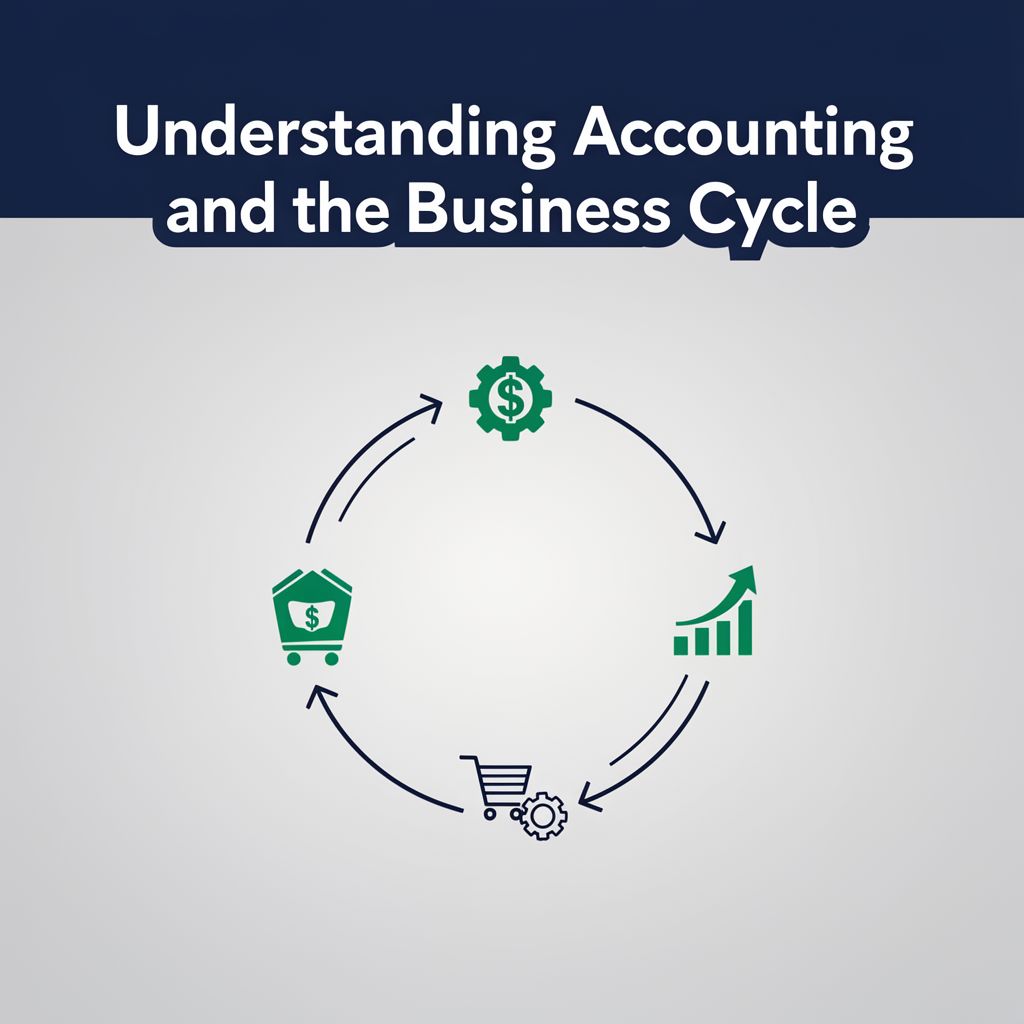

The business cycle represents the continuous operational flow within a company, illustrating how resources are acquired, transformed, and converted into revenue. It is a fundamental concept in understanding how businesses operate and sustain themselves.

The cycle typically follows a continuous loop: Financing ➔ Purchasing ➔ Processing ➔ Sales ➔ Financing (reinvestment)

The overarching objective for company management is to keep this cycle efficient, balanced, and profitable. Effective management ensures that all stages—financing, purchasing, processing, and sales—are meticulously coordinated so that revenues consistently exceed costs, enabling sustainable growth.

Stages of the Business Cycle

Let's delve into each stage of the business cycle in detail:

1️⃣ Financing

Goal: Obtain the necessary funds to start and sustain operations. Use: Financing provides the essential resources to purchase inputs and cover operational costs.

Funds can originate from two main sources:

- Internal Sources: Primarily shareholders.

- External Sources: Banks or other financial backers.

Financing typically takes two main forms:

📚 Equity (Capital Endowment)

-

Definition: Represents shareholders' capital, reflecting ownership in the company.

-

Components: Ordinary shares, preferred shares, savings shares.

-

Repayment: Generally related to net profits; shareholders receive a return in the form of dividends.

-

Rights: Shareholders hold property rights in the company.

-

Providers: Entrepreneurial families, companies (groups or coalitions), investment funds, pension funds, private equity funds, venture capital funds, households' savings, and government shareholdings.

💡 Example - Equity: Three friends invest their own money to open a restaurant: Owner A (€30,000), Owner B (€20,000), Owner C (€50,000). Total capital: €100,000. This is equity financing, meaning it doesn't need to be repaid like a loan. Each owner receives a share of profits (dividends) proportional to their ownership (e.g., if net profit is €40,000, Owner A gets €12,000 for 30% ownership).

📚 Financial Debt (Loans)

-

Definition: Funds borrowed from external parties that must be repaid with interest.

-

Components: Short-term and long-term bank financing, bond loans, leasing, factoring.

-

Repayment: Structured according to contractual expiring dates.

-

Return: Creditors receive a return in the form of interest rates.

-

Rights: Creditors hold specific rights as per their loan agreements.

-

Financial Liabilities: Obligations to financers, which can come from banks, market investors, or other financial institutions through instruments like loans, overdrawn accounts, advances on invoices, leasing, factoring, project financing, and bonds.

💡 Example - Financial Debt: A local bakery secures a €50,000 term loan from Intesasanpaolo Bank at 6% interest over 5 years to purchase a new oven and renovate its shop. The bakery repays the loan with monthly installments of approximately €966 from its sales revenue. This financing allows the bakery to grow immediately, but requires careful cash flow management to cover repayments.

2️⃣ Purchasing

Goal: Acquire the necessary inputs (raw materials, goods, services) for production. Process: Involves the acquisition of production factors, which are the tangible and intangible resources required.

Production factors are categorized by their utility:

-

✅ Fixed Assets (Capital Investments):

- Utility: Long-term utility, useful for more than one production cycle.

- Examples: Buildings, plant & machinery, equity stakes, research & development (R&D), brands.

- Types:

- Operating Investments: Investments in goods and services necessary for production (e.g., plant and machinery, R&D). These generate income only when combined with other production factors.

- Financial Investments: Investments in bonds and equity shares of other companies (e.g., 10% of shares of another company). These generate individual returns regardless of other production factors.

-

✅ Current Expenses (Costs):

- Utility: Short-term utility, useful only once for a single production cycle.

- Examples:

- From Operating Activities: Raw materials, merchandise goods, services/rents/operating leases, wages and salaries, social security contributions.

- From Financing Activities: Interest expenses.

- Non-recurring Items: Extraordinary and non-recurring expenses (e.g., errors, discontinued operations).

- Taxation: Operating income tax.

Outcome of Purchasing: A reduction of cash (e.g., from a bank account) and the generation of a cost, often leading to trade debt.

3️⃣ Processing (Production / Service Delivery)

Goal: Transform acquired inputs into valuable outputs (products or services). Definition: This stage concerns the set of operations put in place to implement the production process. It is an economic transformation, converting the utilities of production factors into the utilities of final products.

The transformation can take various forms:

- Physical Processing: Common in manufacturing enterprises (e.g., raw materials into finished goods).

- Transformation in Space: Moving goods from one location to another, typical for transportation and service enterprises.

- Transformation over Time: Preservation of goods for customers, characteristic of storage enterprises.

4️⃣ Sales

Goal: Deliver goods or services to customers and generate revenue for the company. Process: Involves the transfer of a product or service obtained through the processing of production factors.

Outcome of Sales: Generates cash (e.g., into a bank account) and revenue. It can also create trade receivables (commercial credits) if sales are made on credit.

Sources of Revenue:

- From Operating Activities: Revenues from sales of goods, revenues from sales of services, other operating revenues, capital gain on fixed assets.

- From Financing Activities: Interest revenues, dividends, capital gains on bonds, securities, and shareholdings, other financial revenues.

- Non-recurring Items: Extraordinary and non-recurring revenues.

- Taxation: Tax benefits.

💡 Key Takeaway

The business cycle is a continuous and interconnected loop. Effective management of each stage—financing, purchasing, processing, and sales—is crucial for a company's efficiency, profitability, and sustainable growth. Understanding these stages and their interdependencies is fundamental to comprehending how businesses operate and generate value.